You may have heard the acronym IBC, which stands for the ‘Infinite banking Concept’, or some other version of this—your ‘warehouse of wealth’, ‘building your own bank’, the ‘And One Asset’, etc.—thrown around on podcasts, social media, or maybe even elsewhere in these blogs, and are wondering what it’s all about, and why I think it is one of the greatest financial tools any individual can use. So let this be a somewhat brief—or as brief as I can without boring the poor reader—explanation as to what it is, how it works, and why it matters.

What is IBC?

The Infinite Banking Concept is a term coined by Nelson Nash in his famous book ‘Becoming Your Own Banker’, but in reality, some inarticulated version of this concept has been around for over 150 years. In fact, using this financial vehicle in this way, was a common financial practice of most Americans until the late 20th century; Nelson Nash just helped re-popularize this particular tool, explained how to utilize it to its fullest potential, and improved its marketability.

There are many people on social media, on the radio and podcasts, and all over the internet, who talk about “IBC”, but it is important to note that even the ones that talk about it in a positive light, aren’t always talking about the same thing, (and often either do not fully understand the idea, or even push financial products that are not at all congruent with IBC). Due to this confusion from supposed IBC practitioners, as well as from others who criticize the idea—despite not understanding it, and often mischaracterizing it, among other fallacies—let me first explain what IBC actually is, and what it isn’t.

IBC is a concept that uses a PROPERLY designed whole life insurance company from a top-rated mutual company as a store of capital. This store of capital is then leveraged as your source of credit to reduce the outflow of interest payments to third parties, and eventually allow you to remove yourself from the financial industry altogether if you so choose. Most importantly, this pool of capital is then used to purchase assets and grow your wealth. In addition to this, you receive many other benefits, such as coverage from early death, legacy planning, long term care coverage, retirement planning efficiency (allowing you to fully utilize other market-based assets reducing volatility risk) and much more. What it ISN’T is a typical vanilla 100% base premium whole life policy that you sit and forget, or an over-funded Universal Life Policy, or an Indexed Life policy, some get rich quick gimmick, an “investment” or anything like that.

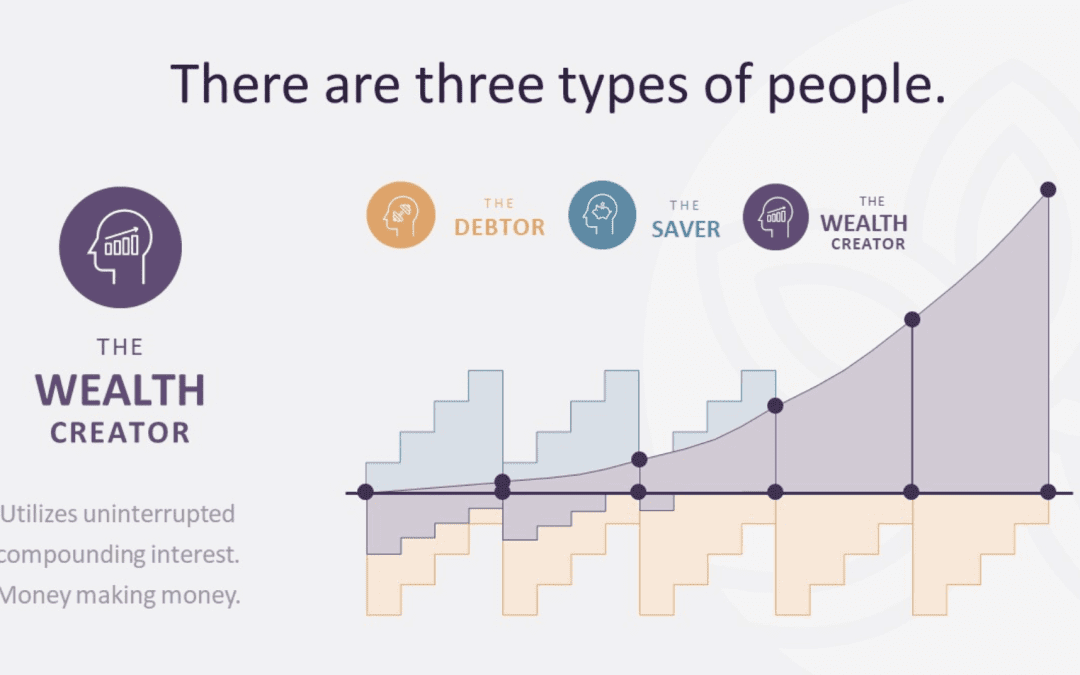

As mentioned, IBC uses a very particularly designed whole life insurance policy, which is not, by itself, IBC. It is simply the base financial tool that IBC is built on. This life insurance product is used due in part to its contractual benefits between the owner and the insurance company. The most important contractual benefits being the death benefit that will be paid out, and the cash value—essentially the equity of the death benefit—that the owner has a contractual right to use during their life via policy loans. This cash value grows every year tax free, and is made up of a guaranteed portion, and non-guaranteed dividend element, and CANNOT decrease in value. In fact, it MUST equal the original death benefit at age 100 or 121. It is the uninterrupted compounding, incredibly flexible loan provision, tax free growth and death benefit, that make it the best store of capital for any individual or family.

The key to IBC though, is putting this capital to work purchasing assets, and flowing the cash flow back into your policy. By doing this you are able to build up your asset base while you never lose out on the compound growth of your capital, thus re-capturing some of the lost opportunity cost of many of the dollars that flow through your hands (and also, just as importantly, not locking your capital up in a government qualified plan where your access is limited, making it ill-liquid). With the same out of pocket outlays you otherwise would have had, you create a large asset that can be utilized in life and in death.

Additionally, there are other less tangible benefits that are arguably of equal importance. As I discuss in my children’s books, the idea of ‘paying yourself first’ is an important concept, and required if you are going to build wealth. Unfortunately, for many people, they are unable to do this, and when they receive those dollars they just as quickly spend them on goods and services, rather than save them. The temptation is just too great to resist.

Additionally, there are other less tangible benefits that are arguably of equal importance. As I discuss in my children’s books, the idea of ‘paying yourself first’ is an important concept, and required if you are going to build wealth. Unfortunately, for many people, they are unable to do this, and when they receive those dollars they just as quickly spend them on goods and services, rather than save them. The temptation is just too great to resist.

What this IBC system helps them do is create a built-in requirement to pay themselves first. Because we are using a properly designed whole life policy as our vehicle, these require certain mandatory premiums, as well as optional premiums, both of which can be set up on automatic payment every month. So ‘paying oneself first’ becomes an automated process, and you no longer see the cash sitting in your checking account earning nothing and waiting to be spent. Instead, it has already been allocated to your savings within the policy, in the form of cash value. From there you are less likely to blow it on useless consumerism, instead you will be more likely to use it wisely purchasing income producing assets and growing your future wealth. This is an incredibly underrated benefit of IBC.

In addition, this IBC system helps you with legacy planning, allows you to more efficiently use your other assets in retirement, and can be used as a superior option for saving for a child’s expected education costs and other expenses.

He who has the gold makes the rules.

But also, he who has the gold finds an abundance of opportunities he otherwise would not have seen or been presented with.

The act of saving has been somewhat disparaged of late (in part due to the government and banking industry fueled inflation over the last 50+ years). Most are told not to save, but instead to speculate, mainly in the stock market. And while there may be a time and place for a little of that, or for the professional stock picker, the act of saving is a vital and underappreciated habit. When you accrue a large pool of capital, you will begin to see that not only are there far more deals out there than you imagined, but these deals can often deliver much better returns than the speculative stocks, etf’s and mutual funds that most are typically throwing their cash at, and can do so with much lower risk and better tax treatment.

When considering a financial vehicle, there are certain characteristics that we would ideally like to see from them. Many of these financial vehicles only have a few of the many traits we would desire. Some of those traits we might want are:

- Safety from loss

- Liquid

- Guaranteed

- Tax free

- No volatility

- Control

- Good rate of return

- Transferable

- Private

These may not be ALL of the traits someone desires, but these are most of them. But when looking at the many different financial vehicles out there, only a properly designed whole life policy from a top rated Mutual company, can deliver all of these characteristics. Thus we use this as our foundation to build our wealth on top of, and secure our individual financial future, and the future of the next generation.

This is by no means an exhaustive explanation of the concept of IBC or whole life, but hopefully it piques your interest. If you want to learn more, check out the books listed on our resource page HERE. Listen to this podcast. And if you have any other questions, or would like to discuss getting your IBC system started, feel free to reach out to me HERE and schedule a Zoom meeting.